Downtown Portland Office

Office leasing guidance for Portland's CBD — building class, transit access, concessions, parking economics, and how to evaluate Downtown against suburban alternatives.

ABOUT DOWNTOWN & CBD

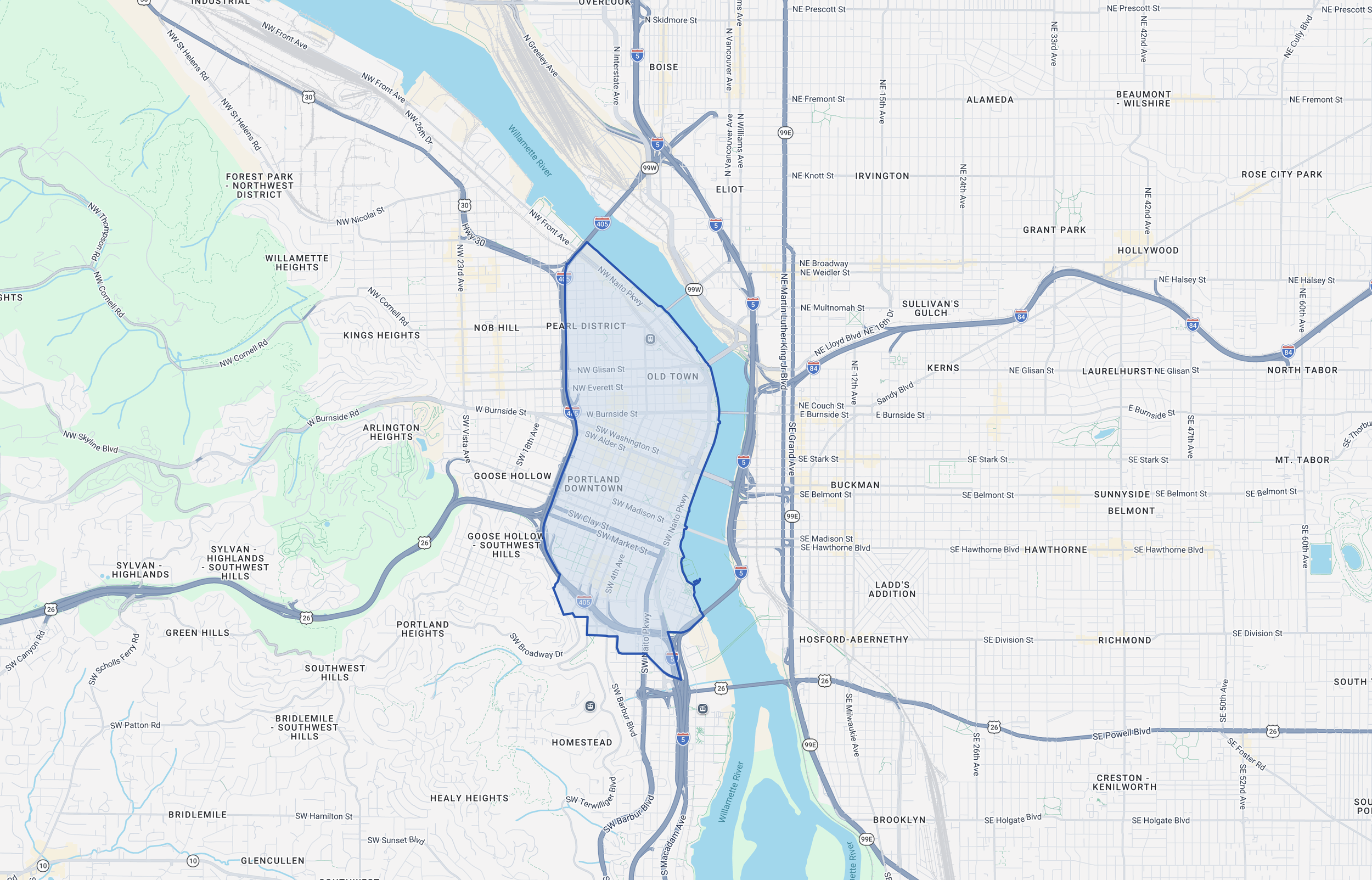

Downtown Portland is the metro's largest and deepest office market, bounded roughly by the Willamette River, I-405, Burnside, and the South Park Blocks. The submarket includes the highest concentration of Class A institutional product in the region, along with a significant inventory of Class B and renovated historic buildings. This page covers what drives leasing decisions Downtown, how to evaluate options by building class and location, and the deal terms that most affect total occupancy cost in the CBD.

The CBD also functions as Portland's legal and financial center — the concentration of law firms, courts, financial institutions, and government offices creates a tenant ecosystem where proximity to other professional services firms is itself a location advantage. For firms in litigation, regulatory work, or institutional finance, being Downtown isn't just a prestige decision — it's a logistical one.

WHAT’S DIFFERENT ABOUT THIS SUBMARKET

Downtown is the only Portland submarket where a tenant can choose between a renovated 1920s building and a modern institutional tower on the same block. That range creates pricing and concession dispersion that doesn't exist in suburban markets. Post-2020 vacancy has shifted leverage toward tenants — concession packages are available at levels that weren't on the table three years ago. But flight to quality is real: the best Class A buildings are absorbing tenants from weaker product, compressing the effective rate gap between classes. Start with parking requirements and building class expectations, then evaluate total occupancy cost.

LOCATION INFORMATION

Downtown Portland / CBD generally refers to the office core bounded by the Willamette River to the east, I-405 to the west and south, and West Burnside to the north. The transit mall runs through the center of the district with MAX light rail, bus, and streetcar service. Major office concentrations cluster along SW Broadway, 5th and 6th Avenues, and the blocks between Pioneer Courthouse Square and the South Park Blocks. The submarket includes Portland's tallest office towers and the highest density of professional services, legal, financial, and government tenants in the metro.

DOWNTOWN/CBD SNAPSHOT

Known For

Strongest transit access in the Portland metro (MAX, bus, streetcar)

Deepest inventory of Class A and institutional-grade office product

Wide pricing dispersion between building classes and concession packages

Post-2020 tenant leverage on concessions, TI, and lease flexibility

Typical User Profiles

Law firms and legal services

Financial services, accounting, and wealth management

Government and quasi-governmental agencies

Insurance, consulting, and professional services

Corporate headquarters and regional offices

Best Fits

Firms that rely on transit-commuting employees

Tenants prioritizing institutional presence and client-facing credibility

Users who need large contiguous floorplates (15,000–25,000+ SF)

Companies upgrading from Class B to Class A during the current concession window

Common Constraints

Parking is limited and expensive — typically 0.5 to 1.5 per 1,000 SF at $150–$250+/stall/month

Building operating expenses vary significantly between full-service gross and modified gross structures

Some older Class B product has deferred maintenance and aging building systems

Street-level conditions and neighborhood perception still factor into some tenants' decisions

RENT, PRICING, AND DEAL TERMS

Typical Deal Terms

Downtown office deals are structured around building class, lease term, and the tenant's credit profile. Concession packages are more aggressive now than at any point in the last decade — landlords in buildings with elevated vacancy are competing on TI allowance, free rent, and rate to attract and retain tenants. Full-service gross is the most common expense structure, with escalations tied to operating expense increases over a base year. Some buildings use modified gross structures where specific expense categories are passed through separately. Parking is almost always priced on top of rent and can represent a meaningful portion of total occupancy cost.

Negotiation Levers

TI allowance and delivery condition: Ranges by building class and term commitment

Free rent: Scaled to lease term — longer commitments unlock more months

Escalation structure: Fixed vs. CPI vs. operating expense pass-through over base year

Parking: Stall count, reserved vs. unreserved, rate caps through the term

Early termination: More available now than pre-2020

Renewal options: Rate reset mechanism matters — fixed, FMV, CPI, or capped

Deal Killers

Parking economics make total occupancy cost uncompetitive against suburban alternatives

Building systems or common areas don't match the tenant's expectations for client-facing space

Expense structure creates unpredictable cost exposure that the tenant can't budget around

Delivery timeline doesn't align with the tenant's lease expiration or business needs

Comparing Proposals

Compare on total occupancy cost: base rent + estimated operating expense exposure + parking (stalls x rate x 12) + TI amortization credit + free rent amortized over term. Two buildings with the same asking rate can price $5-$8/SF apart annually once parking and expense structures are normalized. In the current market, effective rate after concessions is the number that matters — not the asking rate on the brochure.

Mini Case Example

A mid-size law firm evaluating a renewal in a Class B building ran a parallel search across three Class A options Downtown. The concession packages available on Class A product — driven by elevated vacancy and flight-to-quality competition — brought the effective rate within range of the renewal proposal. The firm upgraded building quality, improved client-facing presence, and negotiated a parking package that reduced per-stall cost by structuring reserved and unreserved stalls. The renewal landlord ultimately couldn't match the combination of building quality and economics.

SUBMARKET FAQ

-

Parking is the single biggest variable when comparing Downtown to suburban alternatives. At $175–$250/stall/month for 10-15 stalls on a 5,000 SF lease, parking alone can add $4–$7/SF annually to occupancy cost. Suburban markets typically include parking in the base rent at 3.5–5.0 per 1,000 SF. For firms whose employees drive, the math can make a suburban location meaningfully cheaper even when the base rent is similar. For firms with transit-commuting employees, the parking delta is smaller or irrelevant.

-

Lobby presence, building systems (HVAC efficiency, elevator speed, after-hours access), common-area quality, and restroom/hallway finishes. Class A buildings also tend to have better property management responsiveness and more tenant amenities. In the current market, the effective rate gap between A and B has compressed because Class A landlords are offering aggressive concessions to fill vacancy — which means tenants who assumed they couldn't afford Class A should re-run the numbers.

-

For creditworthy tenants willing to commit to five-plus-year terms, yes. Free rent of 6-12+ months, TI allowances well above historical norms, and escalation concessions are all in play depending on the building's vacancy position. The concessions are strongest in buildings with the most vacancy and weakest in trophy assets with limited availability. The window won't last indefinitely — as vacancy tightens, concession leverage will decrease.

-

Nine to twelve months before expiration for most tenants, earlier for spaces above 10,000 SF or with significant buildout. Even if the plan is to renew, running a parallel search creates the leverage that improves renewal terms. The current market makes this especially valuable — landlords know concessions are elevated and will negotiate harder to retain tenants who demonstrate real alternatives.

-

Full-service gross isn't standardized. Compare base year vintage (a 2020 base year has different economics than a 2026 base year), what's included vs. excluded (janitorial, utilities, management fees, capital reserves), gross-up provisions, and how controllable expenses are capped. Two buildings with identical asking rates can produce different annual cost trajectories based on these structural differences. Request an operating expense history for at least three years from any building you're seriously evaluating.

-

For many tenants, yes. The concession environment has compressed effective rates between classes, which means the upgrade may cost less than expected — or be cost-neutral after factoring in building efficiency, energy costs, and employee retention value. Run the comparison on total occupancy cost including concessions, parking, and estimated operating expenses over the full term before deciding.

-

This is a real consideration for some tenants and it varies by block. Buildings closer to the transit mall and Pioneer Courthouse Square have different street-level dynamics than buildings along the Park Blocks or near the South Waterfront edge. Tour at different times of day. Ask the property manager about building security protocols, after-hours access, and any planned improvements. Some tenants have made Downtown work by choosing specific micro-locations that avoid the blocks that concern them most.

WHAT’S YOUR PROPERTY WORTH?

Whether you're benchmarking against recent office sales, evaluating a hold-vs-sell decision, or preparing for a refinance conversation, a broker opinion of value gives you a clear, comp-based pricing range for your Downtown Portland office property. I'll deliver a comprehensive report covering comparable sales, lease comps, vacancy analytics, and a pricing summary with conservative, probable, and optimistic values — at no cost and no obligation.

ARE YOU PAYING THE RIGHT LEASE RATE?

Whether you're negotiating a new office lease, approaching a renewal Downtown, or evaluating whether your current rate reflects today's market, a lease rate analysis gives you the data to negotiate from a position of strength. I'll pull recent lease comps, concession packages, and vacancy trends for Downtown Portland office space — so you know exactly what tenants like you are paying and where there's room to negotiate.

RELATED

GET IN TOUCH

Contact Matt Lyman at Norris & Stevens about leasing, renewing, or evaluating office space in Downtown Portland. Whether you're a tenant comparing options across building classes, a landlord assessing pricing and concession strategy in the current market, or an investor evaluating acquisition targets in the CBD, share your situation and Matt will follow up with current market context and a recommended approach.

Include your space requirements — size range, parking needs, building class preferences, budget parameters, and timeline — and Matt will respond with current Downtown availability, recent lease comps, and clear next steps.