NW Close-In Office

Office leasing guidance for Portland's Pearl District and NW Close-In — creative space, converted buildings, lease structure variation, and how to evaluate this submarket against Downtown and suburban alternatives.

ABOUT THE PEARL DISTRICT & NW CLOSE-IN

The Pearl District and NW Close-In area is Portland's most character-driven office submarket, centered on the converted warehouse and timber-loft buildings north of Burnside mixed with newer mid-rise construction along the streetcar line. The neighborhood draws tenants who value walkability, design-forward space, and street-level retail and restaurant access — and who are willing to work around tighter floorplates and constrained parking to get it.

This page covers what makes the Pearl and NW Close-In distinct from other Portland office markets, how lease structures and building types vary within the submarket, and the deal terms that most affect total occupancy cost in this area.

WHAT’S DIFFERENT ABOUT THIS SUBMARKET

The Pearl is defined by building character and variety. Converted warehouse buildings with exposed brick, heavy timber, and high ceilings sit alongside newer glass-and-steel construction — and they lease differently. Converted product often has irregular floorplates, limited elevator service, and building systems that are older and less efficient. Newer buildings offer modern systems and more predictable operating costs but lack the aesthetic premium some tenants value.

Parking is the defining constraint. Most Pearl District buildings have limited on-site parking, and what's available is typically priced separately at rates comparable to Downtown. Tenants whose employees rely on driving need to factor parking into total occupancy cost from the start — it can shift the economics significantly against suburban alternatives.

Lease structures vary more in this submarket than in Downtown or the suburbs. Some buildings are full-service gross, others modified gross with meaningful expense pass-throughs. In converted buildings, operating expense exposure can be unpredictable if the building has older HVAC or shared systems. Start by understanding the expense structure and parking economics before comparing asking rates.

LOCATION INFORMATION

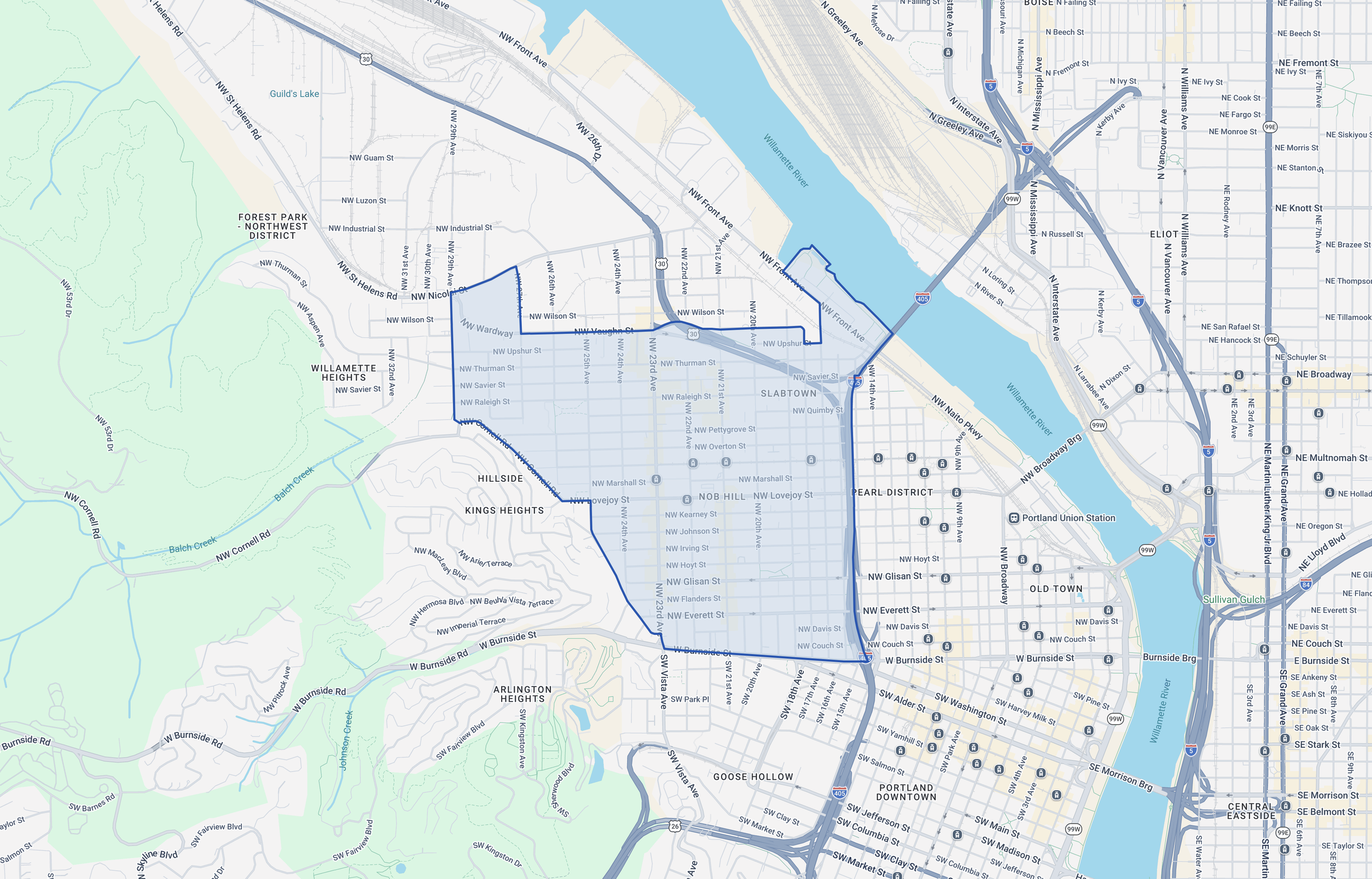

The Pearl District and NW Close-In office submarket generally refers to the area north of West Burnside, east of NW 23rd Avenue, south of the Fremont Bridge approaches, and west of the rail yards and Broadway Bridge. The Portland Streetcar runs through the district along NW Lovejoy and NW Northrup, connecting to Downtown and the South Waterfront. The neighborhood includes Jamison Square, Tanner Springs Park, and dense street-level retail along NW 13th, 12th, 11th, and 10th Avenues. NW 23rd Avenue and the Nob Hill area extend the submarket's western edge with a mix of smaller office product above retail.

CLOSE-IN NW SNAPSHOT

Known For

Converted warehouse and timber-loft office space with exposed brick, beams, and high ceilings

Walkability, streetcar access, and dense street-level retail and restaurant options

Strong appeal for creative, tech, and design-oriented tenants

Wide variation in building type, age, systems quality, and lease structure within a compact area

Typical User Profiles

Tech companies and startups

Creative agencies, design studios, and architecture firms

Marketing and communications firms

Small to mid-size professional services firms

Media and content production companies

Best Fits

Companies competing for younger talent who value neighborhood character and walkability

Tenants who want a non-corporate environment with identity and aesthetic

Firms that can work with smaller floorplates (2,000–8,000 SF typical)

Users whose employees primarily commute by transit, bike, or foot rather than car

Common Constraints

Parking is limited and expensive — most buildings have minimal on-site stalls priced separately

Floorplates in converted buildings are often smaller and irregular

Building systems in older converted product can be less efficient with higher operating expense exposure

Limited inventory of large contiguous blocks above 10,000 SF

Loading and move-in access can be constrained in older buildings on narrow streets

RENT, PRICING, AND DEAL TERMS

Typical Deal Terms

Pearl District and NW office deals are shaped by building type and size. Converted warehouse product often carries a character premium in asking rate, but concession packages and operating expense variability can shift effective economics. Newer construction typically has more predictable expense structures but less of the aesthetic premium. Lease terms range from 3 to 7 years for most tenants, with shorter terms more available in this submarket than in Downtown — particularly for smaller spaces in converted buildings where landlords value occupancy over term length.

Negotiation Levers

TI allowance and delivery condition: Varies widely — converted buildings may have limited TI flexibility due to historic structure or shared systems

Free rent: Available, particularly for longer-term commitments or spaces that have been on the market

Escalation structure: Fixed increases are more common in this submarket than CPI or expense pass-through escalations

Parking: Number of stalls, reserved vs. unreserved, rate caps or fixed pricing through term — this is often the highest-impact negotiation item

Expense structure clarity: In modified gross buildings, negotiate for caps on controllable expenses and clear definitions of what's included vs. excluded

Renewal options: Important in a submarket with limited comparable options — losing a space in the Pearl often means leaving the neighborhood entirely

Deal Killers

Parking economics push total occupancy cost beyond budget when stalls are priced out

Building HVAC or systems can't adequately serve the tenant's space — especially in converted product with shared or undersized systems

Floorplate doesn't support the tenant's layout requirements — irregular shapes, columns, or split levels limit usability

Operating expense exposure in modified gross or NNN structures creates unpredictable cost trajectory

Comparing Proposals

Compare on total occupancy cost: base rent + estimated operating expense exposure + parking (stalls x rate x 12) + TI amortization credit + free rent amortized over term. In the Pearl, two spaces at similar asking rates can price very differently once parking and expense structures are normalized. A converted building at $28/SF with $200/stall parking and variable expenses can cost more than a newer building at $32/SF with parking included and predictable full-service gross economics. Run the real numbers before deciding.

Mini Case Example

A design firm renewing in a converted Pearl District building ran a parallel search to benchmark their options. The renewal proposal came in above market once parking and escalations were factored against newer product in the same neighborhood. By presenting two viable alternatives — one in the Pearl, one in the Lloyd District — the firm negotiated a renewal rate reduction, parking rate cap through the term, and a TI package for a partial remodel. The landlord preferred to keep a long-tenured creative tenant over risking months of vacancy in a niche building.

SUBMARKET FAQ

-

Parking in the Pearl is comparable to Downtown — limited supply, separately priced, and typically $150–$250+/stall/month. The difference is that Downtown tenants usually expect parking to be expensive and factor it in, while some Pearl District tenants underestimate the impact because the neighborhood feels more "neighborhood" than "downtown." For a firm with 15 employees who drive, parking alone can add $27,000–$45,000 annually to occupancy cost. Suburban markets like Kruse Way or the 217 Corridor include parking in the base rent at 3.5–5.0 per 1,000 SF. If your team drives, run the parking math before falling in love with the space.

-

Converted buildings offer exposed brick, timber beams, high ceilings, and architectural character that newer buildings don't have. The trade-offs are real: irregular floorplates that limit layout options, older building systems that can produce higher and less predictable operating expenses, limited elevator service, and sometimes constrained loading and move-in access. Newer Pearl construction offers modern HVAC, predictable expenses, and more efficient floorplates — but looks like newer construction everywhere. For some tenants the character is the point and worth the trade-offs. For others, the operational realities make newer product the better fit.

-

Yes. Downtown is predominantly full-service gross with base year escalations. The Pearl has more variation — full-service gross, modified gross, and occasionally NNN structures exist in the same neighborhood. Modified gross buildings in particular require careful analysis: what's included in the base rent, what's passed through, whether management fees and capital reserves are in or out, and whether there are caps on controllable expenses. Two buildings on the same block can have fundamentally different expense structures. Always compare on total occupancy cost, not asking rate.

-

It depends on floorplate availability and parking. Most Pearl District office spaces are in the 1,500–8,000 SF range. Spaces above 10,000 SF are less common, and contiguous blocks above 15,000 SF are rare. If you need 20+ workstations plus conference and common areas, your options narrow significantly. Parking for a team that size will also be a meaningful line item. The Pearl works best for companies that can fit on a smaller floorplate with a transit-heavy workforce. For larger teams that drive, suburban markets or Lloyd District may deliver more functional space at lower total cost.

-

Both attract similar tenant profiles, but they feel different and price differently. The Pearl is more polished and retail-dense with better restaurant and amenity access. The Central Eastside is grittier, more industrial in character, and generally less expensive — though the gap has narrowed. Parking is constrained in both. The Central Eastside has more zoning complexity (industrial sanctuary overlay) that can limit certain uses. The Pearl has more consistent office product and more predictable landlord expectations. The decision usually comes down to neighborhood identity, budget, and which side of the river your employees prefer.

-

Start 9–12 months before expiration, earlier if you need a specific building type or larger floorplate. The Pearl has limited inventory compared to Downtown, so fewer alternatives mean less leverage unless you start early enough to credibly pursue options in adjacent submarkets. Running a parallel search — even if you expect to renew — is especially important in the Pearl because the landlord knows switching costs are high when comparable options are scarce.

-

HVAC capacity and zoning (can the system adequately heat and cool your specific space, or are you sharing with neighboring tenants?), electrical capacity for your equipment and lighting needs, elevator service and after-hours access, loading and move-in logistics (can you get furniture and equipment into the space?), and the building's operating expense history for at least three years. Converted buildings vary significantly in how well they've been maintained and upgraded — a building that looks great aesthetically can have deferred mechanical systems that drive up costs and create comfort issues.

WHAT’S YOUR PROPERTY WORTH?

Whether you're benchmarking against recent office sales, evaluating a hold-vs-sell decision, or preparing for a refinance conversation, a broker opinion of value gives you a clear, comp-based pricing range for your Pearl District or NW Close-In office property. I'll deliver a comprehensive report covering comparable sales, lease comps, vacancy analytics, and a pricing summary with conservative, probable, and optimistic values — at no cost and no obligation.

ARE YOU PAYING THE RIGHT LEASE RATE?

Whether you're negotiating a new office lease, approaching a renewal in the Pearl District, or evaluating whether your current rate reflects today's market, a lease rate analysis gives you the data to negotiate from a position of strength. I'll pull recent lease comps, concession packages, and vacancy trends for Pearl District and NW Close-In office space — so you know exactly what tenants like you are paying and where there's room to negotiate.

RELATED

GET IN TOUCH

Contact Matt Lyman at Norris & Stevens about leasing, renewing, or evaluating office space in Portland's Pearl District and NW Close-In. Whether you're a creative firm weighing converted space against newer product, a growing company evaluating whether the Pearl still fits, or a landlord positioning a building in a competitive neighborhood, share your situation and Matt will follow up with current market context and a recommended approach.

Include your space requirements — size range, parking needs, building character preferences, budget parameters, and timeline — and Matt will respond with current Pearl District availability, recent lease comps, and clear next steps.

Coverage spans the full Portland metro office market — Downtown/CBD, Pearl District, Lloyd District, South Waterfront, Central Eastside, Lake Oswego/Kruse Way, 217 Corridor, Johns Landing/Macadam, Sunset Corridor/Hillsboro, and Vancouver, WA.